Explore the Vectors Journal

T-RACES

Testbed for the Redlining Archives of California's Exclusionary Spaces

By David Theo Goldberg & Richard Marciano

Programming by Chien-Yi Hou

The residential security maps coded affluent and desirable lending zones green and blue, less affluent and less desirable areas yellow, and zones inhabited by blacks--and so deemed undesirable--with the alarmist, high alert red.

- David Theo Goldberg, Authors' Statement

Alternative views of T-RACES project data:

All info and conversations from this project page

All info and conversations from this project page

http://vectors.usc.edu/xml/projects/iraces_v1.xml

RSS feed of the conversations from this project page

RSS feed of the conversations from this project page

http://vectors.usc.edu/rss/project.rss.php?project=93

http://vectors.usc.edu/xml/projects/iraces_v1.xml

http://vectors.usc.edu/rss/project.rss.php?project=93

|

Video tutorial

Overview of the T-RACES demo site by project author Richard J Marciano |

Conversation

Conversation

Reader-created Threads

Reader-created Threads

Technical Specs

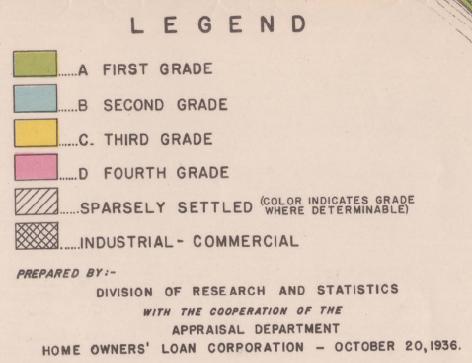

Color Palette

In grading neighborhoods, there are four basic designations:First Grade Areas - "A" (Green)

Second Grade Areas - "B" (Blue)

Third Grade Areas - "C" (Yellow)

Fourth Grade Areas - "D" (Red)

"A" and "B" tend to be caucasian areas, while "C" and "D" tend to represent detrimental and undesirable ethnic groups.

Excerpts of each category follow (in reverse order from "bad" to "good"):

"Yellow areas are characterized by age, obsolescence, and change of style; expiring restrictions or lack of them; infiltration of a lower grade population; the presence of influences which increase sales resistance such as inadequate transportation, insufficient utilities, perhaps heavy tax burdens, poor maintenance of homes, etc. "Jerry" built areas are included, as well as neighborhoods lacking homogeneity. Generally, these areas have reached the transition period. Good mortgage lenders are more conservative in the Yellow areas and hold loan commitments under the lending ratio for the Green and Blue areas."

"Blue areas, as a rule, are completely developed. They are like a 1935 automobile still good, but not what the people are buying today who can afford a new one. They are the neighborhoods where good mortgage lenders will have a tendency to hold loan commitments 10-15% under the limit."

"Green areas are "hot spots"; they are not yet fully built up. In nearly all instances they are the new well planned sections of the city, and almost synonymous with the areas where good mortgage lenders with available funds are willing to make their maximum loans to be amortized over a 10-15-year period -- perhaps up to 75-80% of the appraisal. They are homogeneous; in demand as residential locations in "good time" or "bad"; hence on the upgrade".

— David Theo Goldberg, University of California Humanities Research Institute & Richard Marciano, SILS / University of North Carolina at Chapel Hill, September 15th, 2008